Mortgages.

Mortgages for your property.

Which mortgage is right for me? What are the interest rates? We take care of the important questions regarding mortgages so that your property is optimally financed and the necessary insurance and safeguards for your financial security are in place.

Your advantages:

1 meeting and 1 contact person

Obtain various offers

Development of the optimal financing structure

Review of your family’s protection

Less administrative effort (time savings)

Core concerns of our consultation:

Which mortgage suits your financial and family circumstances?

- Which financial institution is the ideal partner?

- Is your property correctly valued?

- What does the optimal financing look like?

- What is the affordability?

Contact us.

We are happy to advise you.

Adrian Grünenfelder

Position:

Head of Customer Service & Account Manager

Education:

Certified Financial Advisor IAF

FINMA No.:

F01533947

Interests: Even though my connection to Bern is strong, I love traveling the world. Near the beach and ocean, preferably on a surfboard, I enjoy the change of pace. Playing football provides me with a great balance to everyday office life, and I am pleased to represent 360 Consulting AG as a sponsor on the FC Längasse team. |

|

+41 31 911 13 60 |

Pascal Tokar

Position:

Position:

Account Manager & Pension Specialist

Education:

Insurance Intermediary VBV

FINMA No.:

F01463926

Interests: As a certified pension and insurance specialist for SMEs and private clients, I am still delighted every day, even after more than 15 years, to visit my clients and provide comprehensive advice. My extensive experience and network enable me to find an individual solution for every client. Born and raised in Bern West, I moved to Kirchberg in 2020 together with my son and my partner. I keep myself mentally and physically fit with travel, yoga, and plenty of daddy time. |

|

+41 79 628 51 32 |

Sascha Salvi

Position:

Position:

Senior Account Manager

FINMA No.:

F01362783

Interests: For almost 30 years, I have been there for my clients with great passion and enthusiasm. My many years of professional experience enable me to develop and implement optimal solutions. Neutral consultation for corporate clients is one of my strengths. I enjoy spending my free time with my family and friends, whether in pleasant conversation or on a motorcycle tour. |

|

+41 79 301 60 60 |

Financing.

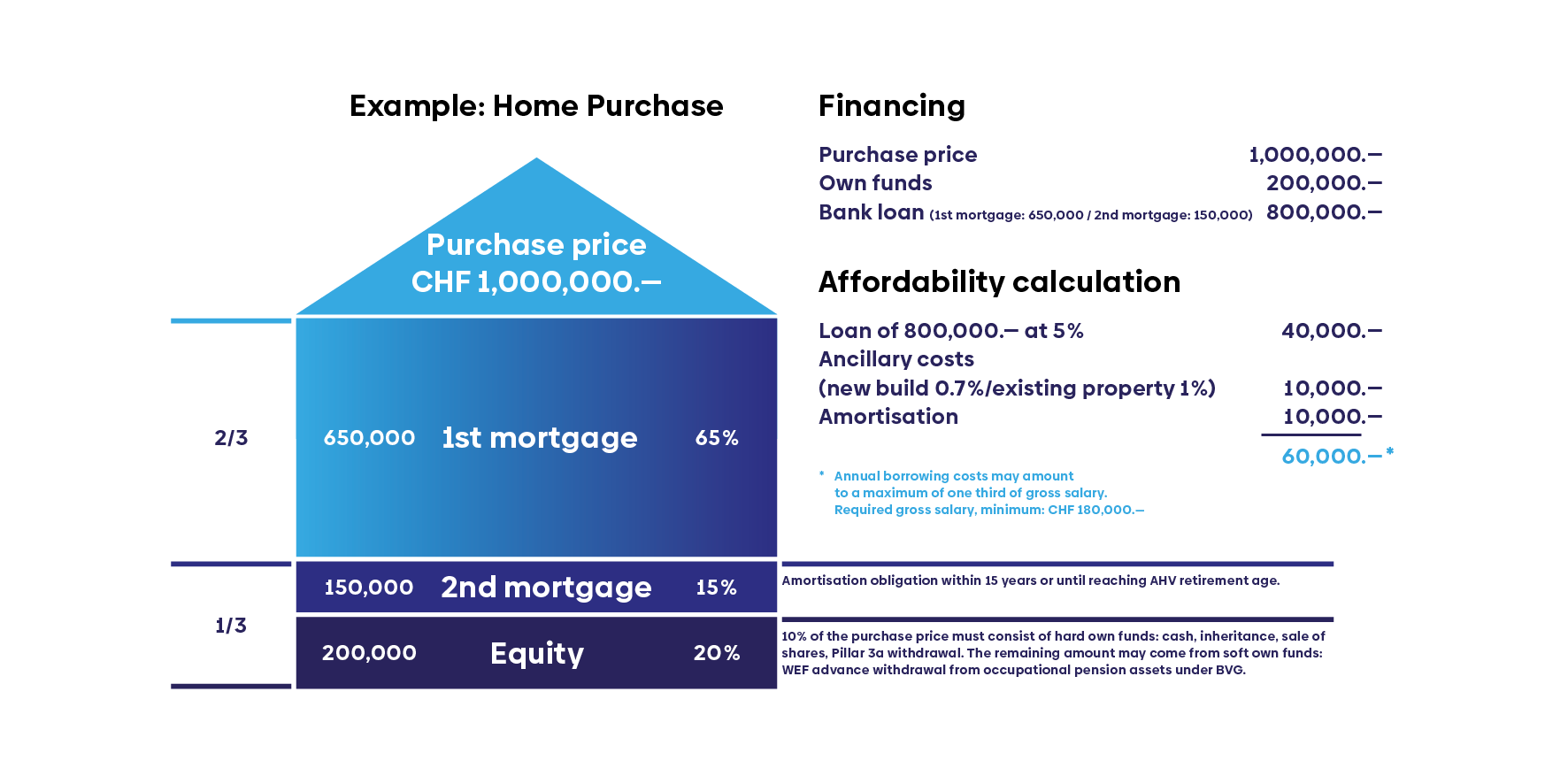

The ratio of costs to income is summarized in Swiss mortgage lending with the term affordability. Both costs and income can be calculated for one month or for an entire year. Mortgage interest, ancillary costs, and amortization payments are counted as costs in the affordability calculation for owner-occupied residential property.

Affordability is usually expressed as a percentage and is also known as the affordability ratio. This is particularly high when income is low but costs are high. A principle that may seem somewhat counterintuitive at first glance. The higher the affordability ratio, the more difficult it becomes for the buyer to bear the mortgage. Since 2014, the Swiss Banking Guidelines have required that affordability for owner-occupied residential property must be based on “sustainable income and expense components.”

If the mortgage interest rate is concluded during a period of particularly low interest rates, increases in this rate must be expected in the future. The affordability ratio must be recalculated when creditworthiness-relevant events have occurred. To estimate the trajectory of income over the coming years, information such as possible job changes or family planning must also be included in the calculation. Most providers set the maximum permitted value of the affordability ratio for owner-occupied residential property at approximately 33%. Annual costs in Switzerland should therefore not exceed one-third of annual income. However, the exact calculation may differ from provider to provider: the calculation is based on either gross or net income, and income from assets, pensions, and secondary income may be credited differently. According to the guidelines, secondary income is only to be credited in the case of joint and several liability.

The capitalized earnings value is obtained when the net income is multiplied by 100 and the quotient is then calculated from the result and the capitalization rate. The capitalization rate is determined taking into account the risk-free interest rate, vacancy or other risk factors, and inflation protection. However, it can be assessed differently by individual companies that bear different risks. This means that the capitalized earnings value can also vary.